Introduction

Bank Runs & Unemployment: What They Mean For The Common Person

Bank runs can be leading indicators of many different economic measures. For one, they can highlight high unemployment which is generally a big negative for the economy at large. On the other hand, bank runs can also be indicators of low inflation. So, while a common person may experience pain upfront from high unemployment due to job loss or job insecurity, it seems that in the near future, inflation will decrease. This ultimately ends up being advantageous for the common person as lower inflation rates mean that goods and services will be cheaper.

Moreover, after inflation decreases, a recession occurs, leading to unemployment ultimately decreasing as the economy improves post-recession. This pattern has been repeated numerous times throughout U.S. history and is a part of the natural cyclical pattern that our economy follows, also known as the boom/bust cycle. Simply put, the boom/bust cycle describes the volatile climate of the economy that shifts between economic expansions (booms) and economic recessions (busts).

Generally, many external factors go into a bank failing and having to shut down, but what does the average person experience after a bank run? This paper includes a quantitative investigation and analysis of how bank runs are associated with volatility in macroeconomic activity–leading to drastic changes in unemployment rates, inflation rates, and CPI indices. This paper also discusses how the average person is most affected by the uncertainty of these metrics.

Method, Assessments, and Measures

The period of 1855-2023 encompasses a wide variety of US economic regulations, consumer habits, and unemployment factors that help to quantify the effect that an average person experiences after a bank run. As mentioned above, yearly inflation rates, consumer price indices, and unemployment data were used as data points to draw inferences on the effect of bank runs/economic downturns on the average person. These measures would allow for a rough estimate of the burden the common person would take on after a bank run.

Furthermore, this is because CPI is a record of the change in prices that a consumer pays for a “market basket of goods.” Inflation helps consumers understand the state of the economy as well as how far their money goes, a concept also known as purchasing power. Essentially, purchasing power is the concept that currency can be valued by the amount of goods and services that one unit of currency can buy. If inflation increases, the value of one unit of currency can decrease.

Unemployment rates, simply put, measure the proportion of people without a job who are currently seeking one against the total labor force. This statistic helps with understanding how many out of an entire population are without a job and are facing all the difficulties that come with unemployment. This is important to note because many people view unemployment as a term meant to describe anyone who doesn’t have a job when it really has a different meaning as discussed above.

The bank runs studied in this analysis are the Panic of 1957, the Panic of 1873, the Panic of 1907, the Great Depression, the Continental Illinois Bank Run, the Great Recession, and the Silicon Valley Bank Run of 2023, However, for simplicity, just three of these bank failures — The Panic of 1907, the Great Depression, and the Great Recession are detailed in this paper through case studies focusing on causes and effects of certain historical bank runs.

Case Studies

The first case study/examination is the Panic of 1907. According to Moen and Tallman (2015), the Panic of 1907 was a result of bad financial decisions and an overall distrust between the public and banking institutions in New York. This was due to an American businessman and speculator causing a huge loss to the banking industry regarding bank shutdowns. One such company that fell was a trust company named Knickerbocker Trust. The major difference between a regular bank and a trust company is the fact that a trust company holds a small percentage of reserves compared to their deposits, leading to a great risk of runs of their deposits. Even though extreme efforts were made by the National Bank of Commerce to avoid the destruction of Knickerbocker Trust, the trust company did eventually fail… but not without setting a strong precedent for how public trust and support are key to the strength of the banking industry.

When people “panic” and withdraw their money from banks on a massive scale, it is due to a public belief that the bank will not be able to return their cash to them. Because banks only carry a finite amount of cash, and accounts are theoretically able to be cashed out on demand, banks essentially “run out of money” during a run on a bank.

So, without a public belief that a bank will be able to return money to its account holders, banks do not function very well. The Panic of 1907 eventually led to the creation of the Federal Reserve System in 1913 which aimed to stabilize the financial systems of the nation, as well as protect consumers by controlling the money supply.

However, at the same time of the Federal Reserve’s creation, and more importantly a massive bank run, unemployment was 2.8%. While this value may look small, inflation was also very painful at 3.7%. This higher inflation rate leads to higher-priced goods and services which have the potential to burden common people.

Bringing context to these values provides a more nuanced understanding of these economic times. Take these numbers into account for what they are: a measure from 1907. The living conditions and average disposable income were much lower than compared to now, which leads to the conclusion that while the Panic of 1907 was not drastically damaging to the American population, it still did impact the economy in negative ways. Inflation is still extremely problematic for the average person as it reduces their purchasing power, affecting all aspects of their affordability of life.

The second case study focuses on the Great Depression, a depression that is widely regarded as the “worst economic disaster in American history” (Richardson, 2013). The stock market crash of 1929 was caused by stocks being carried on margin (the practice of taking out loans to buy more stock than what is possible with cash on hand). When investors, bankers, and creditors realized the stock market was not as healthy and debt-free as they assumed, the stock market crashed. Following directly after was a significant disintegration of the national banking system and equally devastating bank runs.

As a result, the country went through a severe period of deflation after the initial stock market crash (Reed, 2014), with estimates of around a 10.3% deflation rate. Soon after, through government plans such as the New Deal and the Second New Deal, the U.S. government had a hand in fixing the staggering 24.9% unemployment rate, the highest ever in United States history. This had a devastating impact on the American population, with many people losing their life savings, jobs, careers, and much more. CPI did decrease as a result of the heavy deflation the country went through but not enough to significantly help the struggling population afford necessities.

The final case study involves The Great Recession of 2008, also known as the housing crisis of 2008. The U.S. was facing a great expansion in the housing market with home ownership increasing as well as the housing construction market taking off. Many of these new homeowners bought their houses through high-risk mortgages (Weinberg, 2013) which allowed for more people to delve into housing credit. However, shortly after this expansion, the country fell into a recession which led to home prices dropping by almost 20% nationwide (Weinberg, 2013). This set the stage for the financial crisis of 2008 because many mortgage lenders were quite unsure about whether their mortgages would ever be paid back. This uncertainty led to a domino effect of a lack of trust in the economy and housing market, therefore causing a massive recession, “the deepest recession since World War II” (Weinberg, 2013). Unemployment peaked at 9.6% in 2010 and the national inflation rate fluctuated quite drastically showing that the economy was very unstable during this time. This made it harder for the common person to make ends meet due to the high unemployment rate.

Analysis

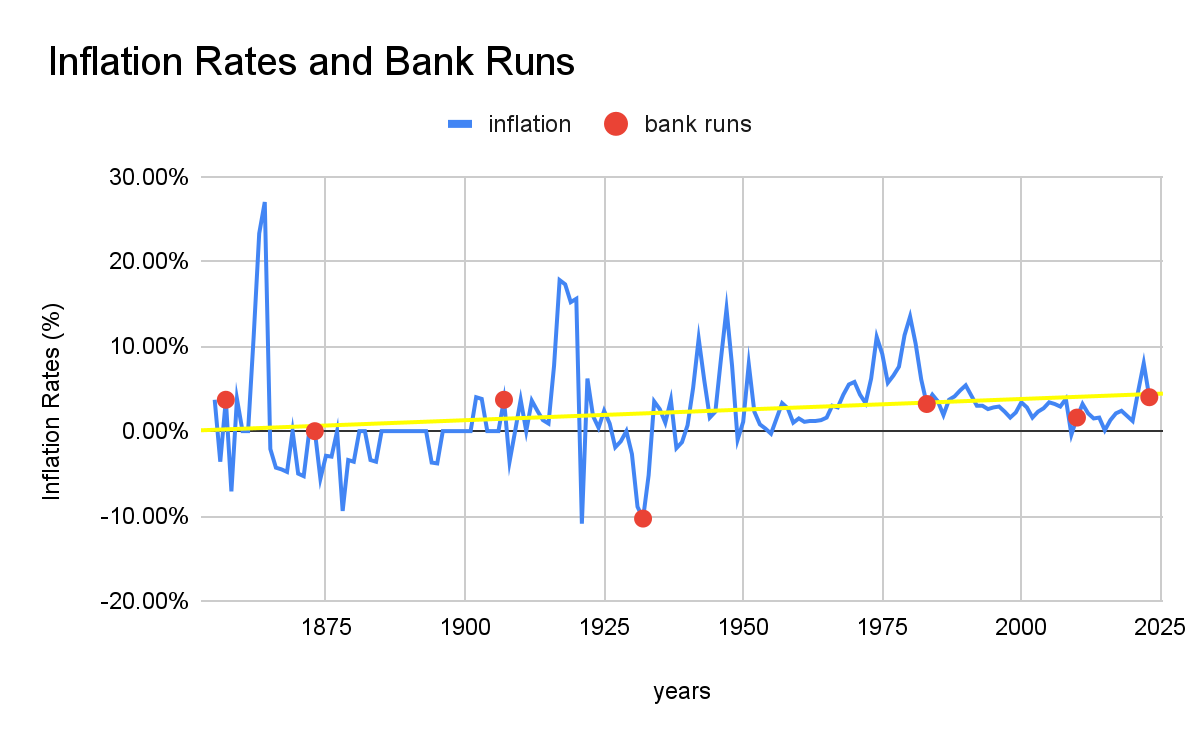

The most vicious thing that follows a bank run is the uncertainty for many people across the country. Their jobs, investments, and assets could be at stake. This is compounded by the fact that bank runs themselves are unpredictable, as they can occur through different/changing unemployment rates, and are primarily based upon consumer trust in the financial market. Shown below is a graph depicting the changes in unemployment rates since 1855. It also highlights the specific bank run years that were used in this dataset.

In the Great Depression, unemployment rates were the highest they had ever been (24.9%), and they had many bank runs associated with it. In contrast, the Panic of 1907 was associated with a very low unemployment rate (2.8%) meaning that bank runs and unemployment rates are not necessarily connected, leading to confusion amongst the general public as to how a bank run could affect their job.

Similar to unemployment, inflation can’t be associated with bank runs, as they have been volatile across the board since 1855. What can be said is that with inflation being unpredictable in terms of bank run data, the common person does not know what happens to CPI and inflation after a bank run. The graph shown below represents the burden the common person in the U.S. would face after a bank run, as it shows the trajectory of inflation rates after the bank runs chosen for this study.

With many bank runs happening around world events, the inflation rate became destabilized, as shown by the Bank Run of 1873 and The Great Depression. The regression line, labeled as the yellow line in the graph, is slowly increasing over the years, also demonstrating how average CPI is increasing over time showing that goods and services are more expensive now compared to 1855.

With CPI data steadily increasing, inflation rates are very unstable. Having an inflation rate this unstable is very detrimental to consumers as they cannot properly gauge the market or the economy for future investments or ensure financial stability. High inflation rates are associated with high unemployment rates, which can have even more of an impact on the vocation and livelihoods of these people.

Discussion

Bank runs are associated with volatility in unemployment, CPI index, and inflation, along with a reduction in macroeconomic activity. This leads to the common person often being heavily impacted in their professional and personal lives.

The most devastating reality of a bank run is its unpredictability. Bank runs can occur during any part of the economic boom/bust cycle and do not necessarily have to be linked to either economic expansions or economic recessions. Thus, consumers can be caught off-guard by bank runs and may not have time to protect their assets and investments.

Due to the unpredictability of bank runs, economic indices such as the unemployment rate, inflation rate, and CPI can also become volatile. Bank runs don’t necessarily happen with high/low unemployment rates or inflation rates making it increasingly important for financial literacy education to take a stand against the often misguided actions taken by consumers after economic devastation.

With these results, better education could be introduced in hopes of reducing some of the devastation that comes with a bank run as well as helping common consumers understand a critical part of their economy and how to best shield against any issues that can come with it. To achieve these goals, more research should be conducted to better understand how bank runs affect a common person and the best strategies and solutions moving forward to protect them.